“When is a car not a car?”

Mobility Ecosystems

(17 minute read)

When is a car not a car? Anyone who has purchased a car in the last few years knows that a car is more a computer on four wheels and that it is more software than hardware.

Technology is rapidly transforming every aspect of the car industry from design to production to sales. Connectivity and Internet of Things means that cars increasingly become seamless, personalised, near-autonomous mobility systems. Fully autonomous cars are not far away but cutting edge software and advancements in driver-assistance technologies from sensors, cameras, safety features, and advanced braking systems make current driving far more pleasant than until recently while also enhancing all aspects of a vehicle’s performance.

In-car features and improvement significantly enrich the car driving experience. Similarly advancements in data analytics, omnichannel marketing, and other digital channels make the process of purchasing, financing, and post-purchase experiences far more enjoyable.

The growing reach and influence of tech in automotive is attracting new players and services who congregate around the industry. Little wonder then that the car industry is also seen less as an industry and more as a mobility ecosystem.

More activity and growth is expected to characterise the mobility ecosystem in the next few years as it evolves and includes non-traditional players. It will feature dramatic changes in consumer behaviours, regulatory environments, and innovation dynamics.

Strategic Underpinnings of the New Mobility Ecosystem

The changing landscape of the new mobility ecosystem highlights some strategic challenges faced by key players. Automotive Original Equipment Manufacturers (OEMs) and suppliers have historically struggled with financial performance owing to structural factors. Their earnings ratios are impacted by high capital expenditures and industry overcapacities.

In this context, many OEMs have strategized about forming alliances within an organised ecosystem that will help them address these challenges through collaboration. The benefits of such a collaboration would include:

- Strengthening core revenue streams by building stronger customer relationships

- Identifying and monetising new revenue streams such as developing tech and integrated hardware-software platforms

- Developing new business models such as data monetisation, pay-per-distance unit payment, platform usage fees etc.

The forerunner for these types of alliances were obviously the digital ecosystems built by Big Tech platforms. Mobility players both established, and newcomers are now trying to replicate this model much to the favour of financial markets.

Key considerations for those wanting to join or develop similar ecosystems are:

- Characteristics of mobility ecosystems

- Opportunities available for mobility players to leverage

- Opportunities to unlock value within the system

Ecosystems and Mobility Ecosystems

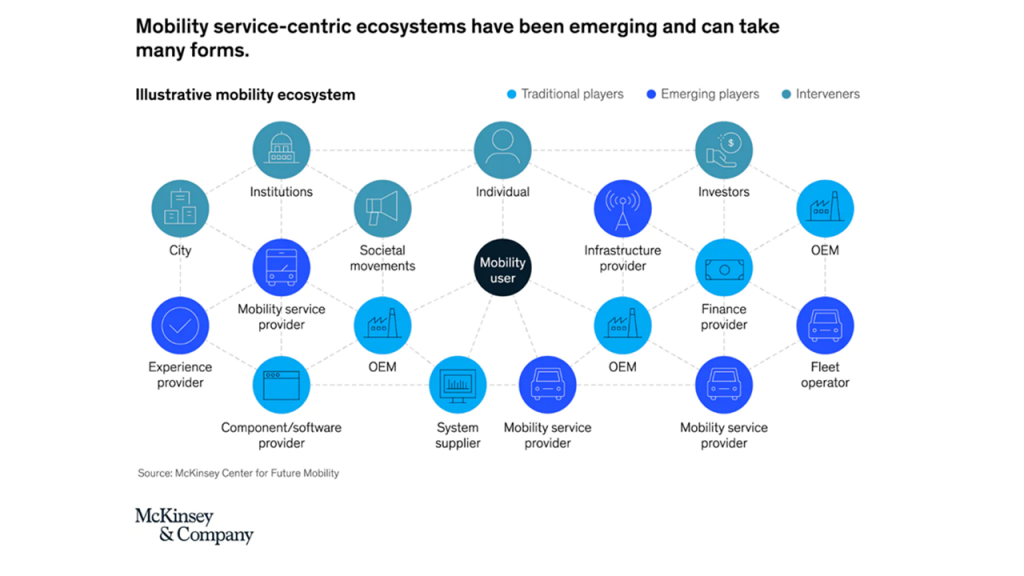

Ecosystems are complex constellations of a variety of players. Digital ecosystems have emerged from industry value chains consolidating. They are networks that bring together players interconnected with an assortment of products, services, solutions and facilitate exchanges amongst players to provide an integrated experience. Information and data is shared and the benefits generated by the ecosystem are shared by all.

Beyond the boundaries of networks and partnerships, ecosystems are beneficial from perspectives of:

- Breadth and diversity of stakeholder groups

- Complementary capabilities that provide opportunities for value creation and capture

- Unified vision aligned by common purposes and aspirations

Mobility ecosystems have similar developmental trajectories. While the needs and preferences of the end users – car owners – are one of the key drivers behind the formation of these ecosystems, private vehicle ownership is only one of several mobility options within the value chain. Many new players who are customer focused are entering this ecosystem positioning themselves in many areas of value capture and creation.

Benefiting from Ecosystems

Within mobility ecosystems, traditional participants like OEMs, suppliers and transport companies benefit from tapping into platform capabilities in many ways. Typically, they benefit from co-opetition, collaborating with erstwhile competitors for developing new technologies, pooling joint R&D investments for reduced risks, and accelerated developments. Ecosystems also allow players to share capital expenditure while developing large scale infrastructure projects. Suppliers also benefit from these relationships by gaining new customers, accessing technologies, and consolidating operations.

Emerging players such as service and infrastructure providers can use ecosystems to expand and strengthen their portfolios, customer relationships, and data accessibility.

Interveners like charities, activists, campaigners, regulators and public authorities can shape the regulatory and wider operating environment through their interventions with the aim of pushing policy agendas and securing industry buy-ins.

Benefits of a Mobility Ecosystem

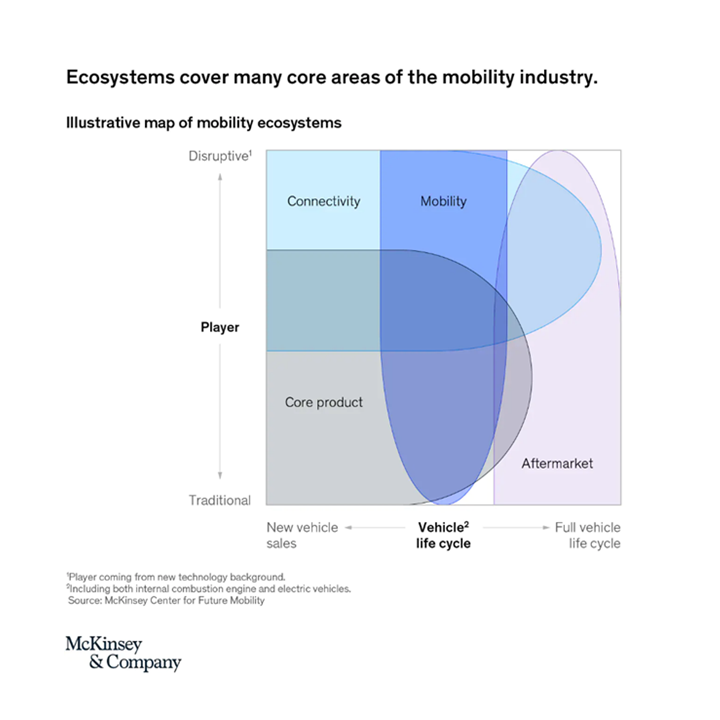

Ecosystems benefit mobility industry in four areas:

Core Product Ecosystems focus on development, production, and sale of vehicles, traditionally the domain of OEMs but with potential for expanding player networks.

Aftermarkets Ecosystems provide services relating to repairs, maintenance, and parts with potential for expanding along the value chain. Increased digitisation may lead to the development of digital, data, and fleet-based ecosystems.

Connectivity Ecosystems form mostly around regional, tech-player-led platforms who operate in areas of vehicle connectivity services, integration and monetisation of user and car data, increasingly a domain of non-mobility players who own control points within the customer relationship.

Mobility Service Ecosystems will cover all transportation options beyond simple car ownership and will include autonomous driving systems, new innovations, and drive traditional players to adapt and integrate digital options.

Players and Mobility Ecosystems

Different players will take different approaches within the system and achieve different levels of success.

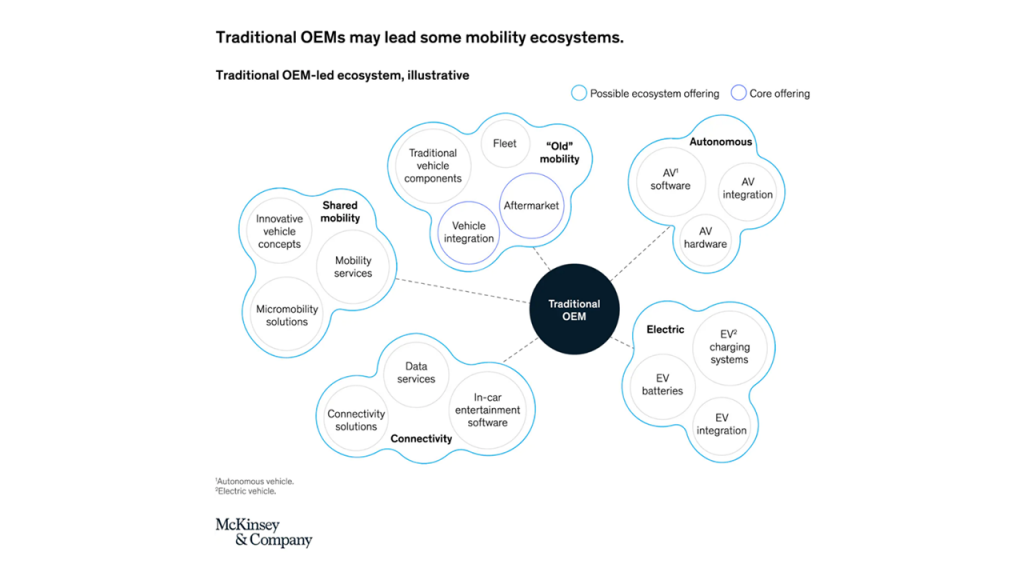

For example, an ecosystem led by traditional OEMs will tend to favour core products but perhaps will explore other business opportunities beyond those core offerings through joint ventures, collaborations etc. These ecosystems (as seen below) will typically tend to support two core offerings in the mobility space: aftermarket and vehicle integration.

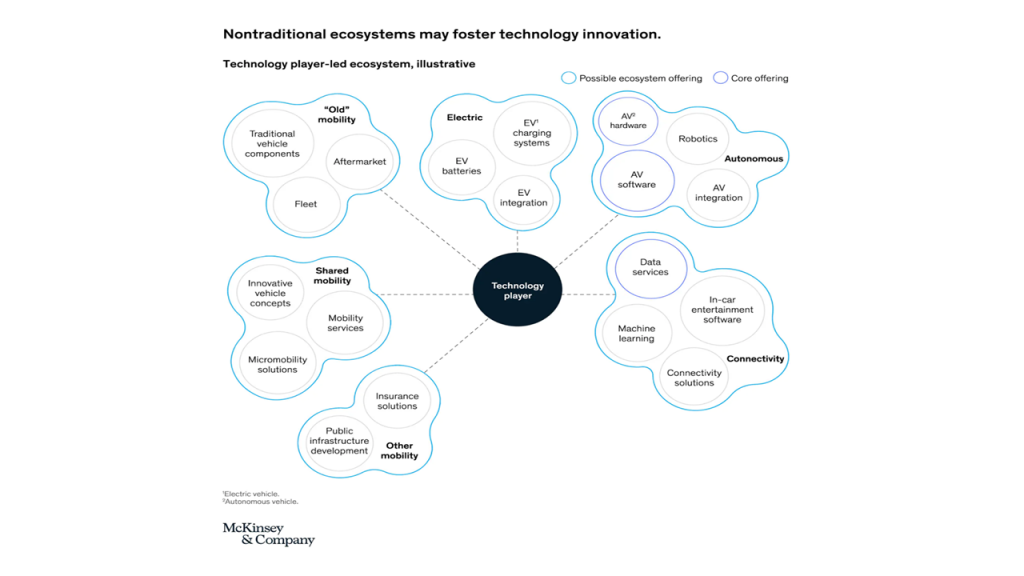

On the other hand, those ecosystems led by non-traditional players like tech companies will be more interested in connectivity and future services. They can leverage their tech competencies and customer reach to approach the ecosystem more sophisticatedly.

Tech-led mobility systems also have the potential to be more disruptive because their participants have a presence across the value chain and beyond into other related and unrelated sectors. Such ecosystems have greater potential for multiple partnerships, extending the value chain beyond vehicles into areas such as autonomous driving hardware, software, and data services.

Ecosystems led by traditional and non-traditional players will be similar in areas of Electric Vehicles (EVs) for instance while they may radically differ in areas of Autonomous Vehicles (AVs), connectivity etc. In the latter area, non-traditional players are more likely to venture into collaborative partnership with other non-automotive players to extend value offerings in areas of data-driven insights, insurance, infrastructure etc. which are typically not areas that traditional players venture into.

Opportunities and Challenges

Many traditional corporations have attempted to pursue opportunities within the ecosystem as creator or collaborator, but with mixed results. Non-traditional players like tech firms on the other hand can hyperscale their platforms to reshape the rules of competition, collaboration, and disintermediation.

Players from outside tech firms have also created strong ecosystems. Notable examples are banks and insurance companies that use data analytics to target customer segments with lifestyle applications and niche products, and telecoms that capture value from health and digital-content ecosystems and data capabilities for both B2C and B2B markets.

All companies need to identify and follow some best approaches and practices in pursuing opportunities within the ecosystem and adapt their business models accordingly.

Rethinking Customer Service

Traditional players must consider their position within the ecosystem and think about how they can deliver value along critical points within the customer journey. This requires companies to go beyond their traditional offerings and reinvent themselves as global ecosystems or networks that can generate around US$60 trillion in revenue by 2025.

Ecosystems also develop in virtuous cycles through network effects. Individual companies can offer customers a greater variety of products and services through ecosystem collaborations that they can never offer on their own. Through collective harnessing of data analytics, they can target better offerings and improve customer experience. When ecosystems expand to cover the entire value chain, they create a customer-centric, unified value proposition in which end-to-end user journeys and a compelling customer experience can be had through a single-access gateway.

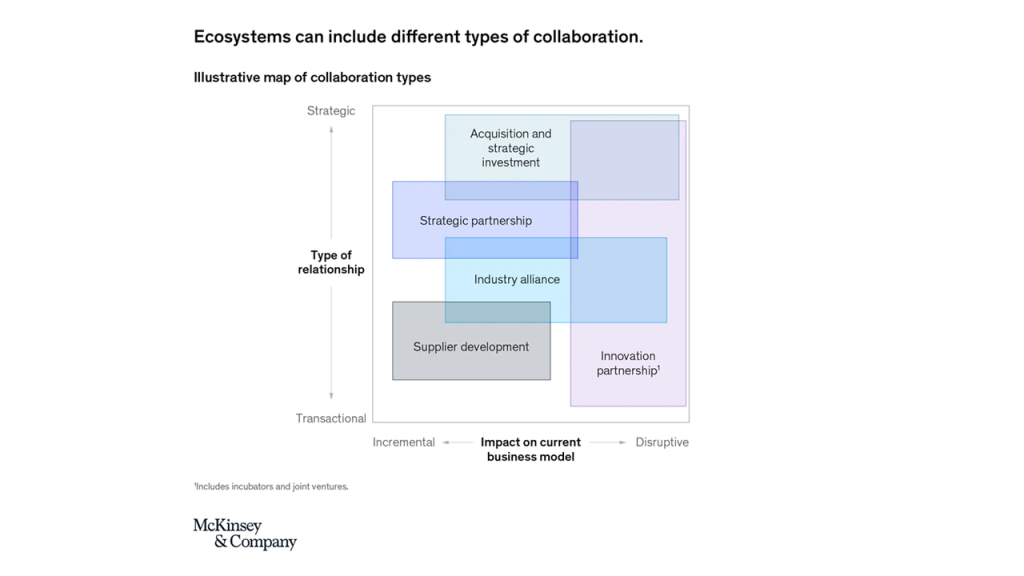

Deciding on the most appropriate approach to collaboration

Players need to decide on creation or collaboration roles within the ecosystem where they can deliver maximum value. Many different types of collaborations can exist within an ecosystem which can range over:

- Supplier-development partnerships for building excellence in the value chain

- Strategic partnerships for close collaboration with partners and mobility players for value creation

- Innovation partnerships such as joint ventures and incubations

- Industry alliances involve multiple suppliers and players

- Mergers, acquisitions, and strategic investments

Any of these options are best approached by how well they reflect and are aligned with the strategic ambitions of players and shaped in breadth and depth accordingly.

Making bold commitments

An ecosystem can only be as impactful as the commitment that players bring to it individually and collectively. They must be prepared to think big in focusing on well curated partnerships of size and scale, always focusing on the customer and building relationships with them, and making bold investments and committing resources where necessary.

Ecosystems will remain fundamental to the future of mobility landscape. In an increasingly complex area, players should bear in mind that:

- Customer centricity will remain critical and unchanging

- Type and range of mobility players continue to evolve

- Technological advancements will not slow down and will only bring previously unimagined possibilities to fruition

Mobility players must be flexible in order to capitalise on the ever-evolving landscape of the ecosystem and capture opportunities for value creation and delivery. The ubiquitous nature of data and digitisation combined with advanced analytics is facilitating new flexibilities. Digital tools enable companies to garner greater customer insights and personalised their offerings in response to changing customer demand.

In addition the best companies will also continue to focus on harnessing technology, building talent, and facilitating collaboration in ensuring that they remain in the best possible position to capitalise on this dynamic mobility landscape.