Nigeria’s Banking Industry after Covid-19

(9 minute read)

Covid-19 has had a huge impact on Nigeria’s banking sector but there are signs of recovery, resilience, and thriving now. This blog looks at some key features of the sector over the past year.

Nigeria’s banking sector is one of the most highly regulated in Africa and forms a critical part of the country’s economy. The pandemic has thrown up some major challenges to the sector.

In response, the Central Bank of Nigeria (CBN) has rolled out a stimulus package that seems to have had a positive impact on the sector in effecting a turnaround.

Existing Vulnerabilities

The pandemic only exposed existing vulnerabilities in the sector and exacerbated them. More than a decade after the financial crisis and about six years after the oil crunch, Nigeria’s banking sector is still feeling the macro-economic aftershocks of these two events. This combined with declining GDP growth rates, rising inflation and unemployment rates, fluctuating currency exchange rates caused by instability in global oil prices meant that a big dampener is being placed on consumption and investment rates and government expenditure.

Policy Measures

Some of the policy measures undertaken by the CBN, while attempting to stabilise the central banking system, has impacted on revenues and profitability of the banks.

For example, CBN’s policy to down-revise electronic banking charges, while ensuring greater protection of consumer rights, caused a huge shortfall in banks’ fees and commission income. Profitability is also being impacted by the country’s Cash Reserve Requirement (CRR) which rates amongst the highest in the world. The CRR requires banks to allocate a huge amount of local currency deposits with the central bank, which in turn restricts their ability to lend these out and earn profits.

Some of these restrictions have had an indirect benefit on Nigeria’s financial landscape particularly in the area of non-banking institutions. Nigeria is widely recognised as one of the most vibrant fintech areas in Africa with annual growth rates of around 200% attracting more local and global investors and showing no signs of slowing down. However, this rate of growth impacts on other areas of the economy such as intense competition for digital talent, a crucial resource for Nigeria’s banking sector.

While the sector’s earnings have shown a healthy annual growth rate over the past decade, actual growth rate in real terms has been significantly lower with much of the growth coming from non-core banking activities like fixed and derivative incomes.

The added impact of Covid-19 has intensified pressures on the banking sector. Lockdowns, remote working, business slowdown, and job layoffs have hit consumer spending and overall economic growth.

The impact is being directly felt within the banking sector in two respects. Revenue income generated through fees and transactions, already slowed because of central policy response measures, have fallen further. Similarly, restrictions on reserve requirements means greater constraints on lending and the added risk of pandemic-induced loan defaults and losses, further impacting on bottom lines.

Digital-driven solutions

Embracing the potential of digital technologies can effect significant positive digital transformation across Nigeria’s banking sector, by way of four key strategic recommendations.

Clearly defining operating segments for scale:

Using the power of data to identify geographical or sectoral segments that have thus far been under-served by the majority of Nigeria’s banking sector would be a way forward. Examples would be the SME sector that have traditionally struggled to access local level micro-financing or businesses located in the north of the country that are under-served compared to the financially better off south. Banks can leverage the power of digital to serve customers within these segments at scale and improve profitability and operating margins.

Transform operating models:

The pandemic has accelerated the push to digital and this trend is set to continue. Combined with the competitive pressures of mobile banking and the fintech landscape and driven by the demands of an increasingly digital savvy consumer, more banks would want to transform their online and digital banking provisions. Paradoxically this would also mean investing in and augmenting customer services as shown by the huge demand for agent banking transactions during the crisis. This is a big cost-reduction opportunity for the sector.

Leveraging data analytics:

Greater leveraging of data analytics, improving digital marketing efficiencies, harnessing the power of artificial intelligence (AI) and machine learning to improve risk assessments, accuracy and efficiency of real-time transactions, and better understanding of customer dynamics would result in a huge improvement in customer benchmarks. This would include customer satisfaction, increase in per capita revenue, and identifying and monetising hitherto hidden marketing opportunities.

Talent management:

Digital skills are going to be critical for all parts of the Nigerian economy but especially so for the banking and fintech sector. Talent scoping, management, and development will be critical for Nigeria and the banking sector would do well to improve employee value proposition of those working in the banking tech sector by competing better for their skills compared to other parts of the wider tech industry.

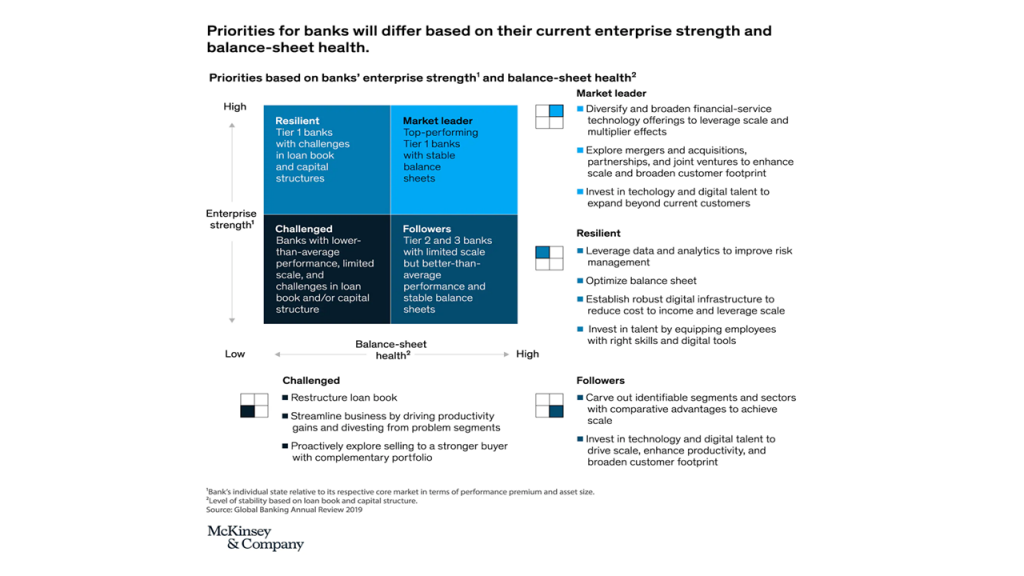

Clearly all of these suggestions won’t apply equally to all banks. Effective implementation of the above measures will depend on a combination of banks’ existing financial and entrepreneurial strength as well as their position in the marketplace. The general principles of the above suggestions should however apply to all players within the Nigerian banking sector if it is to exceed its potential.